This week it was revealed that someone won the $1B Powerball jackpot but has yet to claim it. The single winning Powerball ticket was sold to some lucky person at the Las Palmitas mini market in Los Angeles.

If you won the lottery, how would you spend the winnings? Hopefully, not like most winners since at least one study has found that 70% of lottery winners go bankrupt.

How many times have you heard from family and friends that if they won the lottery, they would stick it in a savings account and live off the interest? But is that really investing? If it is, it’s a losing strategy since inflation will diminish the principal over time. Isn’t the point of investing to grow wealth and not merely to slow its bleeding?

Unfortunately, investment alternatives for large sums of money are often misguided. Putting your money in “safe” assets aren’t usually a wise strategy for growing and preserving wealth but can often be disastrous.

Take Mutual Funds/401(k)’s and the 60/40 strategy, for example. Everyone touts mutual funds and 401(k)’s as “sensible” options for maintaining a diversified portfolio for minimizing risk. The problem is, if the whole market tanks, a diversified portfolio won’t save you from disaster. A 401(k) or mutual fund could be wiped out in months in a stock market crash. So much for your plans of retiring on time or for retiring comfortably.

This scenario happened to potential retirees in 2008, who saw more than 50% of their portfolios wiped out by the stock market crash caused by the subprime mortgage and real estate collapse that led to the Financial Crisis.

What about the 60/40 (60% stocks, 40% bonds) portfolio that Wall Street pushes? Does it make sense to invest $100M using this strategy? The emphatic answer is no.

The 60/40 strategy is outdated. This strategy was devised when bond rates hovered in the double digits and were able to prop up mixed portfolios when stocks dipped. However, based on current low bond rates, bonds are an ineffective counterweight to slumping stocks. There’s recent precedence for the failure of the 60/40 strategy. Rewind to the first half of 2022 when the S&P 500 Index dipped into bear market territory, dropping about 20%. During this span, a portfolio with a 60%/40% mix of stocks and bonds would have declined by 16%.

So where do you invest $100M? Why not ask those investors who have $100M to invest? Suppose you want to know how the ultra-wealthy who have $100M invest; look to the members of TIGER 21.

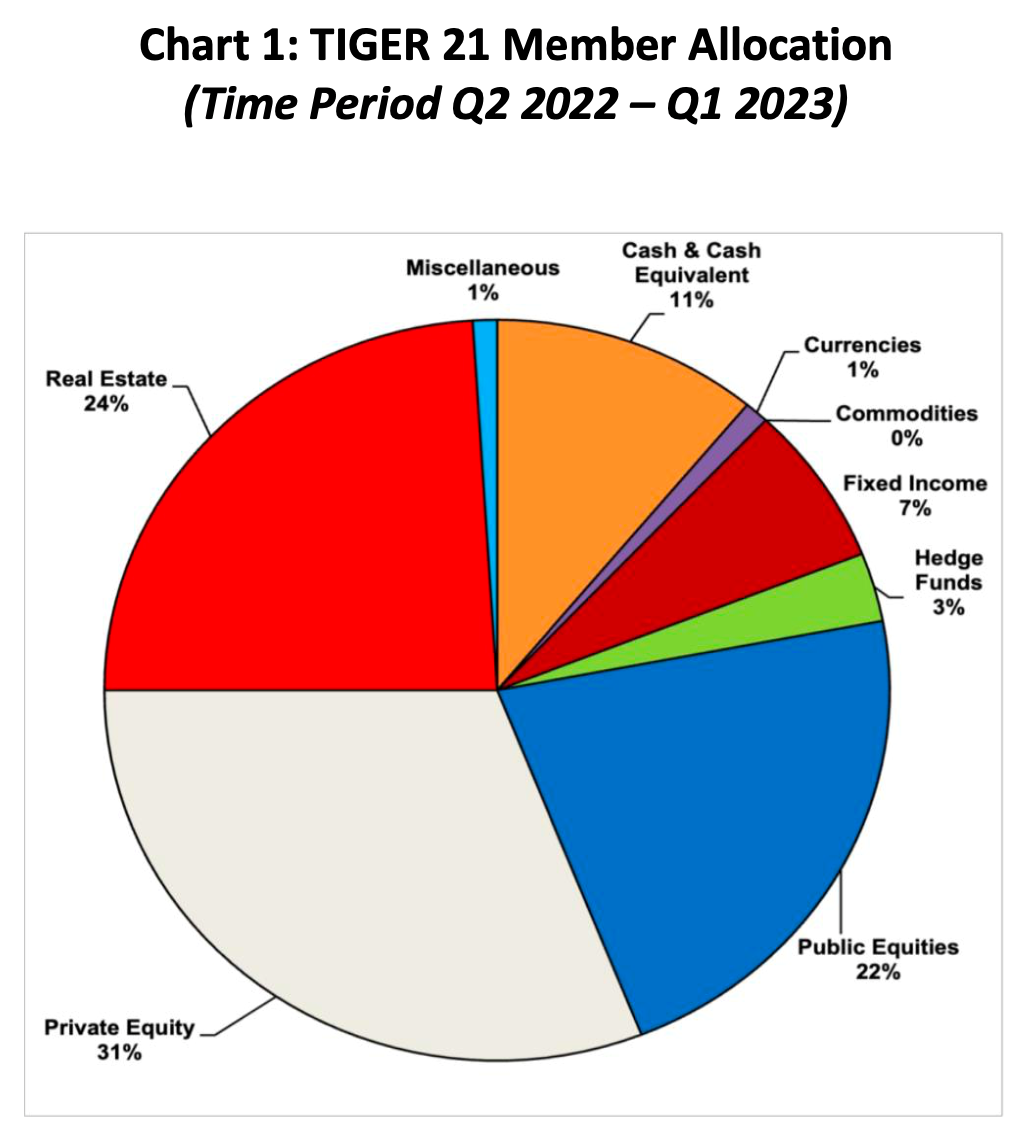

TIGER 21 is a peer-to-peer investing network whose members are required to show $50M in investable assets to join. Many of these members have $100M or more in investable assets. Every quarter, TIGER 21 publishes its Asset Allocation Report showing where its members place their money.

Here is the report from the most recent quarter:

According to the latest asset allocation report, The members of TIGER 21 favor two assets above all else – Private Equity investments (PE) (31%) and Real Estate (RE) (24%).

So why do the ultra-wealthy favor PE and RE over stocks/mutual funds, bonds, and every other asset?

The ultra-wealthy gravitate towards PE and RE because they offer unique advantages for growing wealth free of stock market volatility. They offer above-market returns designed for growing and preserving wealth, not bleeding it like bonds.

While gains from stocks are wholly dependent on unreliable appreciation, returns from PE and RE can be generated from historically reliable cash flow and appreciation. And because these assets are uncorrelated to Wall Street and the broader markets and are tangible, they’re insulated from broader market volatility and shielded from being wiped out overnight.

Now that you have insight into investing $100M, what about $1M? The answer is the same. The investors who have $100M to invest started with $1M or less at one point, and they grew that $1M using the same strategy they still use today to invest their $100M.

Investing in the right assets can turn $1M into $100M.

Whether you have a $100M or a $1M portfolio, the basic tenets of investment remain the same. The key is to do the opposite of lottery winners: Instead of spending first, invest first.

Don’t deplete your capital through excessive and unnecessary expenditures, and grow that capital through investments in the right assets and live off the returns. You have a recipe for growing and maintaining wealth and not for bankruptcy.